THE BIG SHIFT

In today’s business world the game is growth. Ramping up. Getting bigger to get better. Some companies go at it conservatively, in incremental fashion. Other outfits shoot the works. Their game plan aims at exponential growth, and that usually means mergers and acquisitions . . . growing by leaps and bounds . . . combining operations to get maximum market share, economies of scale, payback on technology investments. In other words, major upsizing, in high gear.

WHAT'S DRIVING THIS BIG SHIFT TOWARD DOMINATING INSTEAD OF DOWNSIZING?

Well, it’s that same old one-syllable word: change. But instead of struggling to cope with change, companies now are trying to conquer it. Today’s focus is on building. Buying. And because the world’s new, faster metabolism is catching hold, mergers are back. Sure, shrinking and trimming will continue. We still need to squeeze out costs and soup up performance. But everybody’s doing that.And most folks have figured out that cutbacks, by themselves, won’t make you competitive for long.

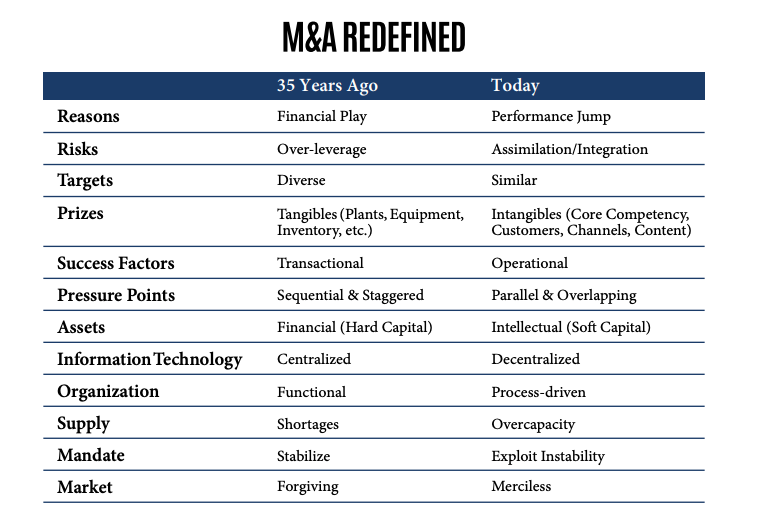

TODAY'S DEALS ARE DIFFERENT.

In the old days, many deals were pure “financial plays.” Today, to a much larger degree, deal success depends on good integration management. The new game mandates operational effectiveness. So growth via mergers and acquisitions becomes a winning proposition only if the companies can be consolidated successfully. And only if the whole truly is greater than the sum of the parts. Or faster. Or cheaper. Or reaches more customers. Financial gains are still the final target, of course, but they aren’t achieved when the deal is cut. Today’s acquirers don’t simply strip away assets and maximize shareholder value in short order. Current mergers are looked at as longer-term challenges.

Another major difference—corporate marriages used to involve much more diverse organizations. Today’s trend is to acquire companies in the same business, or close to it. Firms that complement, that strengthen your capacity to serve customers. Companies vertically or horizontally related. Sometimes your fiercest competitors . . . or suppliers . . . even your customers.

But the risk is still there.

Research shows that related firms are sometimes even harder to assimilate. Why? The acquirer thinks it understands the other business, but often doesn’t. Or maybe both companies have the same types of people with similar skills, and that means redundancy. This is the dark side of synergy.

INSTEAD OF TRYING TO COPE WITH CHANGE, COMPANIES NOW ARE TRYING TO CONQUER IT.

SOFT STUFF IS HARDER TO MERGE

These days acquirers aren’t necessarily hungry for the target companies’ plants, equipment, and other hard assets. Now they’re going after entirely different prizes. The new aiming points are a company’s core competencies. Its customers. Its distribution channels. Its content.

The hot prizes aren’t things—they’re thoughts, methodologies, people, and relationships. Soft goods, so to speak.

Look at how many companies are being bought for their patents, licenses, market share, name brand, research staffs, methods, customer base, or culture.

And here’s the scary part. Soft capital, like this, is very perishable. Very fragile and fluid. Unlike machinery, real estate, inventory and other tangibles, you can’t lock it up at night. Nor can you sell it to someone else if it somehow gets away from you.

So you’ve got to nurture these soft assets. You must seduce them into the new combined enterprise with great care and then protect them. This takes tremendous skill.

TODAY'S DEALS REQUIRE MORE FINESSE. THEY AIN'T YOUR DADDY'S M&A.

Related Articles